Where Do We Go From Here?

Signal Definer: Weak. The S&P 500 squeaked by with a barely-positive return, and the bond markets were largely positive, marking the first positive month of the year for most sectors.

Where Do We Go From Here?

Signal Definer: Weak. The S&P 500 squeaked by with a barely-positive return, and the bond markets were largely positive, marking the first positive month of the year for most sectors.

The S&P 500 Index returned 0.01%

The Bloomberg U.S. Aggregate Bond Index returned 0.64%

Fed Funds Target Range: 0.75 – 1.00%

The May economic releases captured the ongoing story: A strong labor market, slowing but positive growth, an expanding manufacturing sector and declining but still strong consumer confidence. All of this would seem to indicate an economy that can weather rate increases without tumbling into a recession.

Except that everybody seemed to think the opposite.

Let’s get into the data:

The Fed’s coordinated reassurance of a 50 basis point hike at the June and July meetings, combined with the mid-month inflation release that showed CPI declining slightly, ultimately served to alleviate concerns that the Fed would move even more aggressively. In some quarters, it raised hopes that the Fed would move back to a 25 basis point increase in September, or even pause rate increases, if labor markets continued softening and CPI trended down.

So much for that. The spike in headline CPI from a 0.3% increase in April to a 1% increase in May was the largest since 1981. At the June FOMC meeting, The Federal Reserve raised the key short-term interest rate by 75 basis points, for the first time since 1994. The June increase will likely be followed by either a 50 or 75 basis point increase in July and another increase in September.

Besides the upward spike in CPI, among the data that the Fed looks at is the expectations for inflation going forward. Inflation tends to be a self-fulfilling prophecy, where consumer expectations for inflation in the future result in higher inflation.

The most recent University of Michigan consumer sentiment survey said that the public’s expectation of inflation five years from now jumped to a reading of 3.3% from 3% in May. That was the first increase since January. Expected inflation a year from now also ticked up, hitting 5.4% versus 5.3%.

Will the moves work on inflation? Or will we end up in recession or stagflation? The Fed does have a strategy:

In the Summary of Economic Projections, the Fed indicated an unemployment rate of 4.1% by 2024. Powell acknowledged the increase in his remarks, but stated that the number is historically low, and that achieving the joint goals of low unemployment and inflation on a downward path to 2% would be a “successful outcome.”

As of early June, Q1 2022 earnings season is mostly complete, with over 97% of companies reporting. Of 489 issues, 377 beat operating estimates (77.1%), while 350 of the 486 (72.0%) have beaten estimates on sales. Earnings for the quarter were expected to decline 12.7% from the Q4 2021 record and be up 4.4% over Q1 2021. For 2022, earnings are expected to set another record, increasing 7.5% over 2021.

The 10-year U.S. Treasury ended the month at 2.85%. Intra month, the key rate reached 3.21%. This marks the first time this rate has been above 3% since December 2018. The Bloomberg U.S. Aggregate Index was up, returning 0.64%. As represented by the Bloomberg Municipal Bond Index, Municipal bonds returned 1.48%. High yield corporate bonds were positive, with the Bloomberg U.S. High Yield Index returning 0.24%.

The US High Yield market returned 0.24% in May, bringing the YTD return to -7.74% as measured by the ICE BofA US High Yield Constrained Index (HUC0). Signs that the Federal Reserve would be flexible in rate hikes led to a rally later in the month. BBs rallied first and outperformed for the month, while Bs and CCCs lagged.

In the alternative credit markets, a recent report from S&P Global Market Intelligence looked at the evolution of private credit and compared the asset class to more liquid options in the face of the ongoing market volatility. “The volume of high-yield bond issuance has plunged this year in the face of market volatility. That’s not unusual when equity markets swing wildly. But private credit providers, still flush with cash, have swooped in, underwriting transactions that may have been done in the traditional high-yield bond market in the past.” The report also addressed a shift to larger deal sizes in the private credit space: “In recent months, private credit providers have increasingly taken down larger deals that in the past would have been done in the syndicated loan market.”

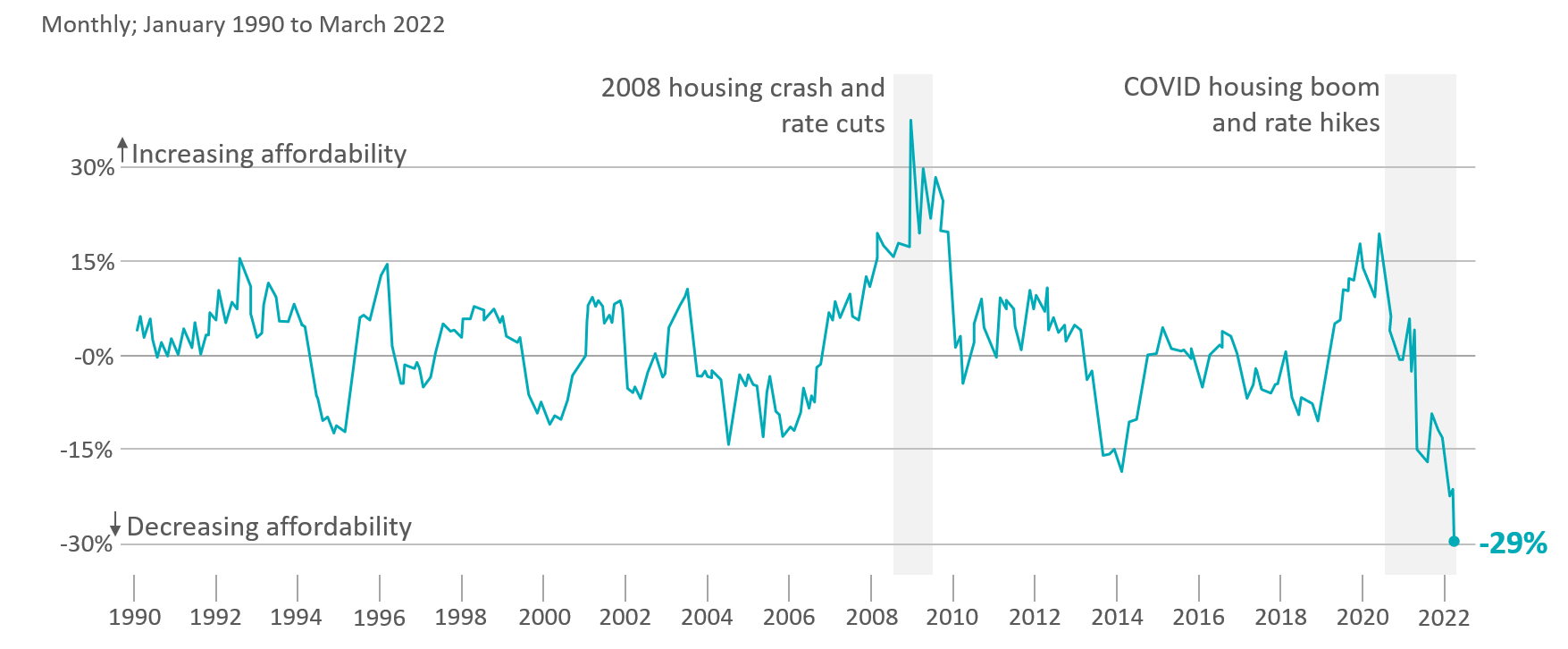

National Association of Realtors Home Affordability Index

The combination of higher mortgage rates and higher home prices has led to a drastic decrease in the affordability of home ownership.

Source: FactSet; Chart: Erin Davis/Axios Visuals

Source: Atlanta Fed; Bureau of Labor Statistics; Axios

The Evolving Investor Mindset and What It Means for Advisors

Read More >>Sign-up for The Signal, a monthly rundown of what moves took place in the credit market and our latest educational and thought leadership content.

CION will use the information you provide to be in touch with you and provide updates. Feel free to change your mind at any time by clicking the unsubscribe link the email you receive. We will never share your information and will treat it with respect.