Private Debt: Not Your Average Asset Class

Let’s Level Set: What is Private Debt?

You’ve likely heard of private debt, or at the very least seen headlines in the news. And for good reason; since 2011, private debt has been the only private asset class to grow fundraising yearly, including through the pandemic.[footnote val="1" id="1"] Preqin reported assets under management exceeded $1.6 trillion in 2023, and forecasts that private debt AUM will grow at a CAGR of 11% between 2022 and 2028 to reach an all-time high of $2.8tn in 2028.[footnote val="2" id="2"] And in terms of all alternative asset classes, private debt is forecast to be the fastest growing over the next four-to-five years.[footnote val="3" id="3"]

Private debt refers to loans made to private companies by non-bank lenders. The companies are usually described as the “middle market,” with revenues between $10 million and $1 billion. Because of their size, they often cannot access the public markets to raise capital. The non- bank lenders are generally asset managers who have developed an expertise in originating these types of loans; meaning they research the market, the companies, and the financial prospects, they perform extensive due diligence and are experts in structuring the loans.

They loan out the capital and usually hold the loan until maturity. Because the loans are illiquid and the companies have no other sources of capital, the loans tend to have higher yields than the public markets. Sometimes, these loans can provide lower than expected default risk because of the extensive due diligence, and can possibly recover more if they do default, due to the specialized knowledge, experience, and flexibility of the lender.

What is the Appeal?

Private debt appeals to those who may want to consider income-producing assets in their portfolios. In past decades, U.S. Treasury securities or corporate bonds were often the go-to asset, and portfolios holding 40% of their assets in bonds, the “60/40” portfolio, were considered the norm. However, the last several years have seen higher volatility, and higher correlations between stocks and bonds, which has meant that the traditional 60/40 may not meet investors’ needs.

Private debt has the ability or generally tends to have higher returns than traditional fixed income assets, with volatility only slightly higher than investment grade bonds. Private credit also tends to have higher yields than other assets as these companies are not able to access other sources of funding. They also offer an illiquidity premium, as the loans are usually longer-term investments. The enhanced yield may be as much as several hundred basis points over traditional bond yields.

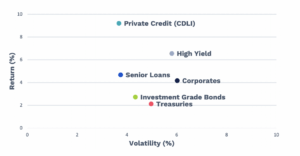

Risk and Return (15 Years Annualized)

Source: Zephyr Analytics, Cliffwater Direct Lending Index. All data is annualized over 15 years ending September 30, 2023, unless otherwise indicated. “Private Credit” is represented by the Cliffwater Direct Lending Index (from inception on September 30, 2004 – September 30, 2021). “Senior Loans” is represented by the S&P/LSTA Leveraged Loan Index. “High Yield” is represented by the Bloomberg High Yield Index. “Corporates” is represented by the Bloomberg US Corporate Bond Index. “Investment Grade Bonds” is represented by the Bloomberg US Aggregate Bond Index. “Treasuries” is represented by the Bloomberg US Treasury Index.

As the chart above shows, adding private credit to a traditional portfolio may help to lower risk and increase overall portfolio return. With equity market volatility increasing and traditional bond performance struggling in the face of rising rates, a source of lower volatility that is not correlated to the equity markets can help to smooth portfolio returns. Since private credit is not traded on public exchanges, correlation to equities is low. In addition, private credit loans are typically structured as floating rate instruments. Yields tend to increase as rates rise, allowing them to keep pace with inflation and avoid interest rate risk.

Where is Private Debt Headed?

According to a recent survey by The Lead Left, quoted in Institutional Investor, 95% of institutional investor respondents expect to maintain or increase their allocations to private debt in the next 12 months.[footnote val="4" id="4"] With inflation spiking, and interest rates increasing, the floating rate nature of private loans may be helping to increase demand. And because it is not traded on public exchanges, private debt offers much lower correlation (in some case none) to traditional assets.

With equity volatility increasing and traditional bonds struggling, private credit may help to provide ballast to an equity position in a portfolio. This can provide a source of true portfolio diversification and can help to lower portfolio volatility over time.

Why Businesses (Borrowers) Are Turning to These Alternative Lenders

Borrowers are increasingly turning to the private credit markets, even at the upper end of the valuation scale where they can potentially access bank funding or public markets. This is because going to a private lender, rather than a bank, can allow for greater customization of loan structures, including longer maturity profiles to match their financing needs.

Because these lenders are often asset managers with access to flexible capital, they can often conclude deals with greater speed, and the borrower has a greater assurance of the deal being completed. An article in the

National Law Review posited that “Today is arguably a golden era for this asset class, as the traditional banks, battered by the financial crisis and subsequent increased regulation, have progressively shied away from certain types of risk and been forced to operate without the flexibility over terms and capital structuring offered by private credit. Contrastingly, private credit managers have become more sophisticated, as they are able to participate in a wide variety of complex structures and less traditional business types, offering flexibility on terms, and greater speed of execution and pricing.”

To Lend Well Requires Very Specific (Manager) Skills

We talked about the illiquidity premium that private loans can provide. There is also a complexity premium, in that the manager must have a very high degree of expertise to compete in this market. Originating loans often requires thorough review and analysis.

Having a track record demonstrating that a manager has avoided meaningful defaults and losses and consistently selected performing loans creates a virtuous circle. The more loans a manager makes, the more companies they see, the more selective they can be.

The Value of Patient Capital

The above-referenced article goes on to discuss what happened during the pandemic, as established private credit asset managers were able to work effectively with their portfolio companies to support them and help them navigate through the crisis. “Private credit worked proactively with existing clients, underscoring the strength and value of relationships and partnerships with their clients. It wasn’t just the size or execution capability that was impressing everyone, it was the true nature of patient capital, and the flexibility, willingness, and creativity in structuring that provided borrowers with real solutions.”

The Bottom Line

As the democratization of investing and lending continues, investors looking for income-producing assets and struggling with the lack of yield in the public markets may want to expand their horizons to include private debt as part of their credit allocation.