A Changing Game: Income Funds Deserve a New Look

What Are Income Funds?

Income funds are just what they sound like, an investment vehicle that focuses on assets that provide an income stream, either through dividend payments or coupon payments. In some cases, they can also be viewed as total return vehicles that provide some growth potential through capital appreciation along the way.

While that may sound pretty simple, income funds are deserving of a deeper look. The reasons to use them in a portfolio have changed, the investor pool has expanded, and the types of assets that they invest are evolving.

From a Specific Audience to Mass Appeal

Retired investors have reached a life stage where they need a dependable source of income to provide money to fund expenses, and to preserve capital so that it may last out retirement. Preserving capital, as opposed to growing capital, requires lower portfolio volatility. This group is the traditional investor base for income funds. As retirement gets closer, investors were often advised to transition their portfolios into a 60/40 mix of equities and bonds, which was often an increase in the credit side of the portfolio from the 80/20 or 70/30 mix that younger investors may deploy.

This approach has generally worked but has struggled in recent years as persistent low yields has made finding income challenging. However, the environment for bonds over the past several years has created a difficulty on the performance side as well.

From a portfolio allocation standpoint, the changing investing landscape and the availability of new types of investments in income funds have transformed them into an investing style that provides utility while considering asset allocation goals, timeline, and income needs.

Diversification has become more important, and harder to find

Equities and bonds have been inversely correlated for the last few decades, but with high inflation and an active Fed raising rates, they have become more correlated. This means the traditional role of the 60/40 portfolio, in which equities and bonds together smoothed volatility, has not been as useful to investors.

While the traditional method of constructing a portfolio with an income-driven sleeve may not be working, there are options. Funds with innovative structures that allow for investment in alternative assets are experiencing demand.

An Evolved Landscape: How Income Investing Has Changed

Some of the biggest changes have been seen in the credit space. Traditionally, investors accessed income assets through the public markets by buying Treasuries or corporate bonds. Over the last several decades, the amount of income these assets provide has declined precipitously as yields have trended lower and lower.

So where are investors seeking income? Investors are increasingly considering alternative assets. A study of investment advisors found that they turn to alternatives to potentially reduce risk, enhance returns, and provide an uncorrelated asset to other portfolio holdings in order to increase diversification and lower volatility in client portfolios. While there are many different alternative strategies, such as private equity, hedge funds, and venture capital, which would generally be regarded as growth strategies, the same study found that a significant percentage of advisors responding (36%) are using alternatives on the income side of the portfolio as well.

And within income alternatives, the private markets are eating up a lot of the new inflows. Private debt generally refers to non-bank institutions, such as asset managers, making loans to private, middle market companies that because of their size, cannot access the public markets to raise capital. These loans may offer a yield premium over public market debt because they tend to be illiquid; they are not traded on exchanges and the manager may hold them until maturity.

Preqin reported assets under management exceeded $1.6 trillion in 2023, and forecasts that private debt AUM will grow at a CAGR of 11% between 2022 and 2028 to reach an all-time high of $2.8tn in 2028. [footnote val="1" id="1"]

What Else Are Investors Considering?

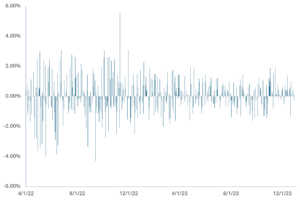

Equity market volatility is increasing, making it even more important to seek sources of return that are not overly correlated to equities. A long-term asset that can both throw off income and provide relatively uncorrelated returns may help to maintain a preferred risk/return profile. Additionally, the availability of more diverse income-producing assets makes these types of funds deserving of a new look.

S&P 500 Daily Percentage Change

Source: Barechart S&P 500 Historical Data

Wrapping It Up

Whether you build a portfolio on your own, or you work with a financial professional, taking stock of your investments is always a good idea. Income funds are a modern way to gain access to income without liquidating assets, and can also provide exposure to alternatives. There are of course risks involved, as there are with any investment, so be sure to understand them thoroughly, either by the reading the prospectus or the offering documents.