With Direct Lending,

Deal Selection Is Where It’s At

The resiliency of private credit during economic downturns has demonstrated the fundamental qualities of direct lending. The potential to recover quickly and post positive returns despite market volatility, combined with the enhanced yield generally offered by these types of loans have resulted in increased demand from investors. An uptick in asset gathering and the entrance of more asset managers into the space has followed.

But are more players a good thing? The reasons for the resilience are deeply rooted in the structure of the deals and the lenders’ competence. The size and number of deals have increased, but sometimes at the cost of loosening deal terms, as lenders compete to deploy “dry powder.”

Given the current environment of policy shifts, geopolitical instability, and uncertainty around the future of interest rates, experience matters as much as access to capital. As the pressure on companies increases, it is even more essential to take a critical look at what can potentially increase the success of a private credit transaction.

Favorable deal terms aren’t just about enhanced yield. The ability to rigorously monitor and take action when necessary are both crucial to helping companies ride out economic downturns. And only the strongest managers can insist on both and bring deals to close quickly.

A THRIVING MIDDLE MARKET LOOKS FORWARD

The decline in the number of public companies is well documented. The number of public-company listings in the United States peaked in the mid-1990s, at nearly 6,000, but that number has fallen by about half over the past 20 years.[footnote val="1" id="1"] The number of IPOs has generally remained stable over the last two decades, as companies are able to remain private longer.

The middle market, where most private credit loans are made, refers to companies with between $10 million and $2 billion of revenue. There are approximately 200,000 of these companies, and their combined annual revenues total more than $10 trillion, which represents approximately one-third of the U.S. economy.[footnote val="2" id="2"]

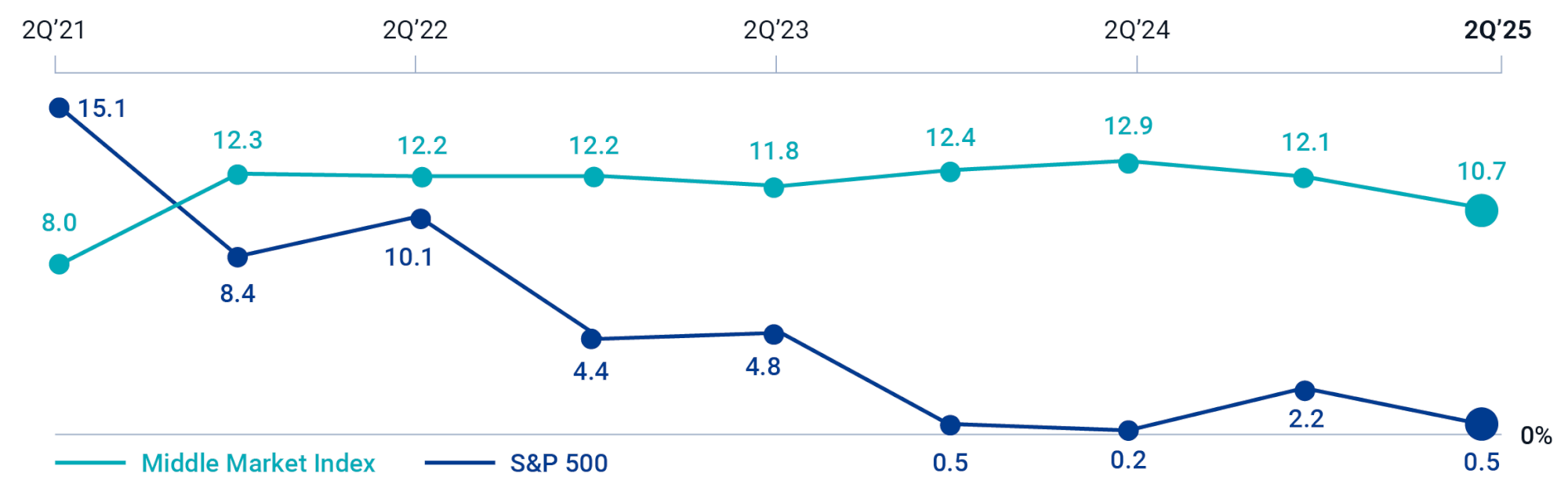

The National Center for the Middle Market reported a growth rate of 10.7% for 2Q’25 in the Mid-Year Middle Market Indicator. According to their 2025 executive summary, “throughout the post-pandemic period (Q4 2021 – Q2 2025), middle market companies have reported an average year-over-year revenue growth rate of 12.4%.”

Revenue Growth Rates (%)

Source: National Center for the Middle Market / The Ohio State University Mid-Year 2025 Middle Market Indicator

A second quarter survey by KeyBank found that 72% of middle market executive respondents have a favorable outlook for their company’s financial performance in the next 12 months. Additionally, KeyBank’s July 2025 Middle Market Sentiment Report finds that “even with shifting policies, tariff unknowns, and mixed market signals, leaders appear ready to ride out turbulence.”This speaks to the confidence in these companies’ business prospects and a potential need for capital, which is largely sourced through private debt.

AN UPWARD TRAJECTORY OF ASSET GROWTH

When it comes to private alternative assets, private equity has long led the way. But in the last decade, the credit side of the equation has been scaling massively and rapidly. Bank lenders, the traditional source of capital, have greatly reduced their role. Non-bank lenders, such as asset managers that focus on private credit, have stepped into the funding gap and created a thriving asset class.

These private credit managers have long track records in the space, and significant relationships with middle-market companies. They also have deep reserves of capital and on-the-ground teams across the globe that can underwrite deals effectively, efficiently, and quickly. As the asset class has grown and shown resilience through economic downturns demand from investors has moved beyond institutions and now includes individual investor portfolios. This is resulting in increased fund raising.

Changing Dynamics Driving Growth of Private Credit

Source: Financial Times, Preqin, The Wall Street Journal, February 2025

Source: Financial Times, Preqin, The Wall Street Journal, February 2025

DRY POWDER IS CHANGING DEALS

The rapid growth of the asset class has meant that asset managers are amassing capital. While deployment has been steady and the amount of invested assets is growing, the levels of capital available for investment have increased.The top 20 global private credit fund managers collectively hold more than 35% of the dry powder in the space. These managers have long operational and investment histories and have been building relationships for decades, so may have less difficulty deploying capital.

Newer managers who have been attracted into the space but do not have the operational expertise and relationships of these pioneers may experience more challenges. They are seeking a competitive edge to attract borrowers and may, in some cases, find it by loosening deal terms.

Private Credit Dry Powder ($B)

Source: S&P Global, January 16, 2025.

Source: S&P Global, January 16, 2025.

According to S&P Global and Preqin as of January 2025,

“The top 20 global private credit fund managers collectively held more than one-third of dry powder available to the asset class as demand for nonbank lending continued to grow.”

THE IMPORTANCE OF DEAL SELECTION

Private credit managers who consistently and effectively deploy capital have a specific profile, often developed over decades of underwriting and investing. The ability to be very selective in deal choice is the province of managers who have cultivated these attributes. They can be nimble and can craft a portfolio across multiple dimensions and factors.

It’s not just about size. While these managers may often participate in very large deals, the overall goal is to create a portfolio with enhanced yield and a manageable risk profile. It’s about the right size, company, industry, and deal metrics to make an investment for the long-term designed to hold up in various environments, while meeting portfolio goals.

- Breadth and depth of presence. The concept of “boots on the ground” matters in making these types of investments, as they must be rigorously and comprehensively researched and analyzed – both before and after investment.

- Reach, contacts, and a reputation for getting deals done, so they are often first choice and see almost every deal that comes to market.

- The ability to work with a borrower across the entirety of their lending needs. The ability to underwrite first and second lien loans, as well as unitranche loans, may provide a competitive advantage.

- Generally have long track records and work with the same companies in repeated transactions. For lenders, skewing new originations towards companies they know well and that have an established borrowing record can mean higher quality deals.

- Strong relationships with other sourcing partners.

WHY THE DEAL STRUCTURE MATTERS

Private debt deals are governed by “covenants” on the loan. These are specific deal terms that limit the actions of a borrower and allow the lender to have oversight and a degree of enforcement. If a company (borrower) breaches or violates a covenant, it can trigger other provisions or even penalties.

Covenants are put in place to make certain that the interests of the lender and the borrower are aligned. This allows the lender to remain involved throughout the life of the loan, and when issues arise due to economic downturns or other issues, the lender can help the company to get back on track and potentially avoid a default on the loan.

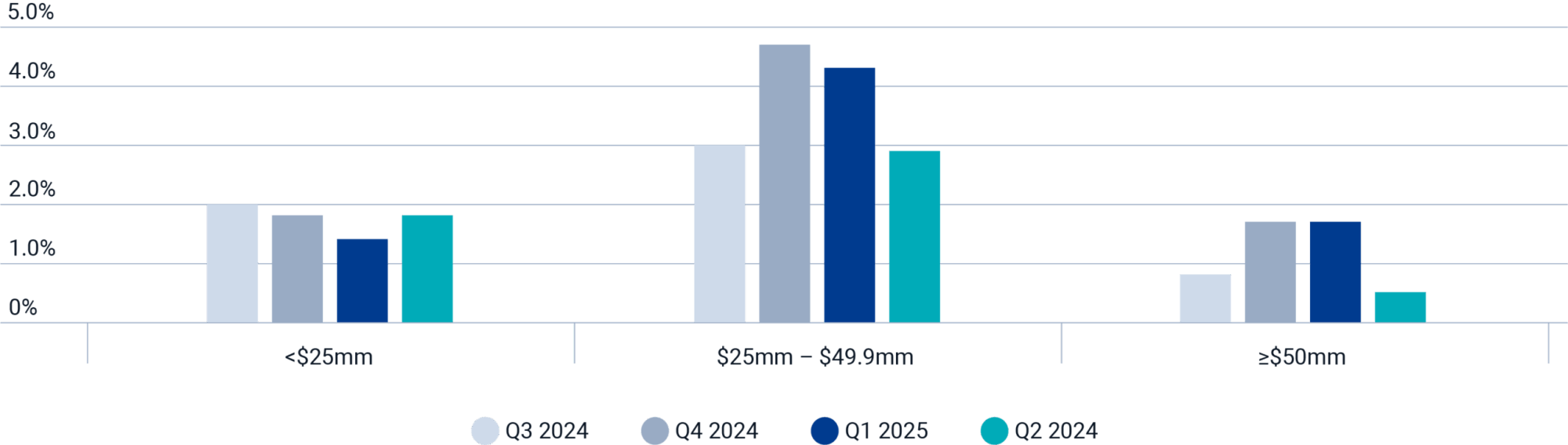

Recent Default Rates

Source: Proskauer Private Credit Default Index, July 23 2025.

WHY ARE COVENANTS EFFECTIVE?

Covenants are written into deals to help manage risk for lenders. They are enforceable and breaching a covenant can result in penalties and even default.

They limit the actions the borrower can take

They specify the amount of oversight that the lender has

The goal of a manager is to work effectively with a borrower to prevent defaults. Covenants are essential to creating a legal structure to monitor company finances, prohibit the borrower from taking on additional debt, and provide the manager the opportunity to work with the company to mitigate problems if financial distress occurs. Strong covenants can provide early warning signs of potential default, limit additional borrower debt, and create priority over junior lenders.

CHARACTERISTICS OF SUCCESSFUL MANAGERS

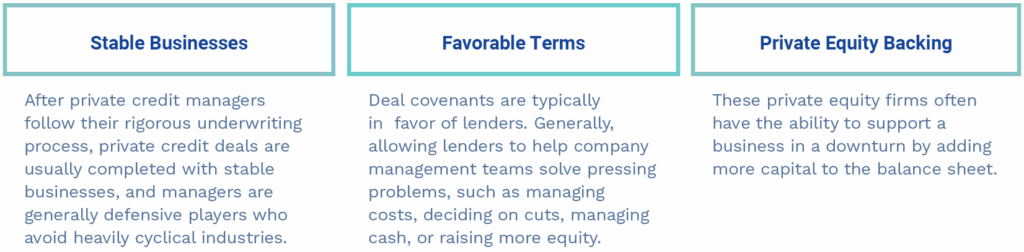

Institutional Investor took a look at why private credit was able to navigate so successfully through the pandemic, and found several common reasons among private debt managers.

Besides the attributes listed below, these were managers who had already deployed capital based on strong underwriting procedures, knowledge, and expertise on how to structure and manage direct lending deals. They had the ability to select from among the strongest companies and quickly close larger deals with companies on the upper range of the middle-market spectrum.

A criticism of the growth in private credit prior to the events of 2020 was that the asset class had never been tested by a broad-based credit event that would ripple across the entire economy. The resiliency of private credit throughout the pandemic helped to address that line of criticism.

SOME MANAGERS ARE UNIQUELY POSITIONED TO CAPITALIZE ON A GROWING ASSET CLASS

Economic uncertainty continues, and we now have geopolitical uncertainty and shifts in economic policy. Interest rates may fall, but the timing of potential rate reductions is uncertain. Managers who stick to direct lending principles that emphasize defensive non-cyclical industries may see outperformance. Private credit loans are generally structured as floating rate notes, which means they tend to have low durations, which can help to mitigate interest rate risk.

In an uncertain environment, credit selection becomes even more paramount. Investment managers must choose borrowers in a strong position to manage their liabilities, while also underwriting these loans with protective features such as covenants, call provisions, and low debt-to-EBITDA multiples.

Footnotes

[disclaimer-footnote val="1" id="1"] McKinsey & Company. Insights. October 21, 2021. [disclaimer-footnote val="2" id="2"] Keybank. Middle Market Sentiment Report. July 2025

Risks As with any asset class, there are certain risks associated with non-investment grade debt and private credit. Credit risk is the risk of nonpayment of scheduled interest or principal payments on a debt investment. The risk of default may be greater. Should a borrower fail to make a payment, or default, this may affect the overall return to the lender. Further, illiquid investments and private credit require longer investment time horizons than other investments. For these and other reasons, this asset class is considered speculative and may not be suitable for everyone.

All investments carry a certain degree of risk, including possible loss of principal and there is no assurance that an investment will provide positive performance over any period of time. There are specific risks associated with investing in various types of financial assets and in different countries. The information contained within should not be a person’s sole basis for making an investment decision. One should consult a financial professional before making any investment decision. Investors should ensure that they obtain all available relevant information before making any investment. Financial professionals should consider the suitability of the manager, strategy, and program for their clients on an initial and ongoing basis.

The information contained within is for educational and information purposes ONLY. It is not intended nor should be considered an invitation, inducement to buy or sell any security or a solicitation to buy or sell any security. The information is not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from us or any of our subsidiaries to participate in any of the transactions mentioned herein. This is also not intended to be a forecast of future events nor is this a guarantee of any future result. Both past performance and yields are not reliable indicators of current and future results. Information contained herein was obtained from third party sources we believe to be reliable; however, this is not to be construed as a guarantee to their accuracy or completeness. Observations and views contained in this report may change at any time without notice and with no obligation to update.