The Private Asset Revolution Is Here

Private assets on the equity and credit sides of capital raising have been growing over the last two decades, fueled by an ability to adapt as the economy, regulatory environment, and markets have evolved.

Institutional investors with long-term investment horizons have recognized the potential advantages of private assets compared to the public markets for decades.

Illiquid private assets may provide the opportunity for enhanced return, yield, and portfolio diversification. The resilience of these assets through major market disruptions has added to the appeal.

Individual investors seeking to expand traditional 60/40 portfolios with alternatives are the next frontier in the growing demand for these assets.

Flexible structures can now provide access to long-term investment strategies while allowing limited liquidity.

The evolution of these two asset classes mirrors our changing economy, and private equity and private debt have played vital roles.

As we enter a new phase of the business cycle, companies with private equity backing who seek private debt capital may be uniquely positioned to manage through difficulties.

The Background

Private debt has always been the “little brother” to private equity, but it is catching up quickly.

Since 2011, private debt has been the only private asset class to grow fundraising yearly, including through the pandemic.[footnote val="1" id="1"] Preqin reported assets under management exceeded $1.6 trillion in 2023, and forecasts that private debt AUM will grow at a CAGR of 11% between 2022 and 2028 to reach an all-time high of $2.8tn in 2028.[footnote val="2" id="2"] And in terms of all alternative asset classes, private debt is forecast to be the fastest growing over the next four-to-five years.[footnote val="3" id="3"]The Growth of Private Debt ($bn)

Source: Financial Times, Preqin, The Wall Street Journal

Source: Financial Times, Preqin, The Wall Street Journal

What Is Private Debt?

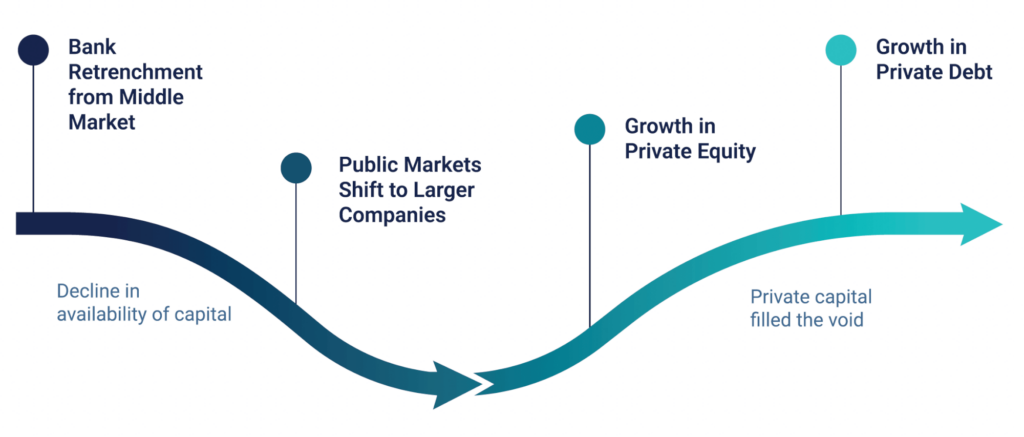

Private debt, also called private credit, encompasses several strategies. The largest by far is direct lending to privately held middle market companies. These companies historically accessed bank funding for capital needs, however, banks have been exiting this market for decades, leaving a void that private lenders have filled. This was accelerated by regulatory changes after the Global Financial Crisis (GFC).

The Characteristics of Private Lending

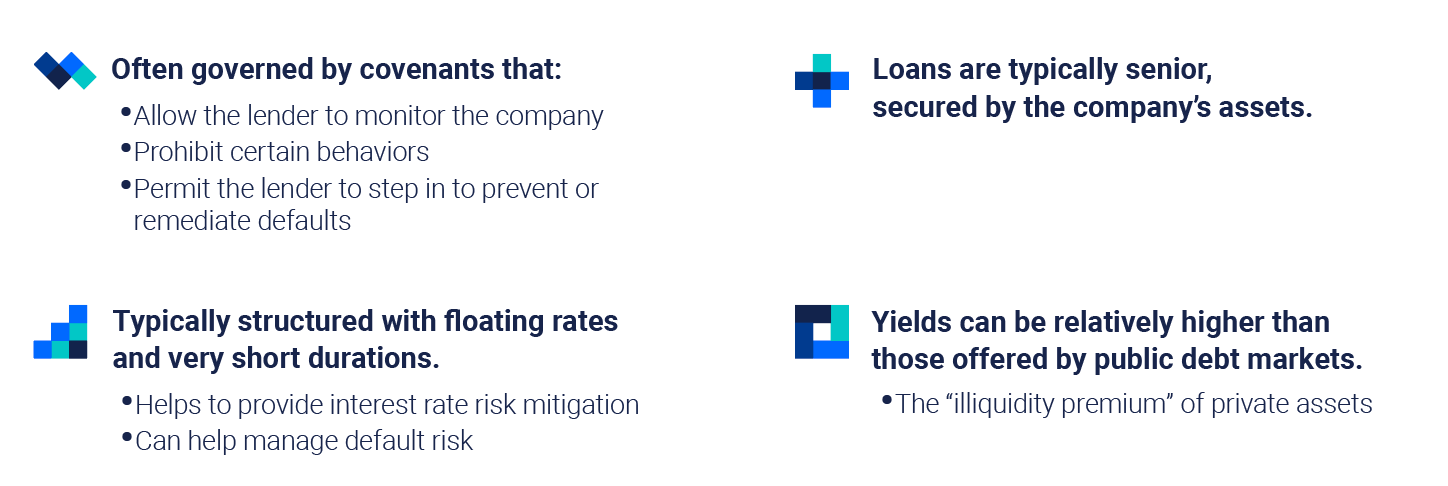

These loans are direct agreements between the company as the borrower and the private debt lender. They have several characteristics:

Why Is the Partner So Important?

The original impetus for middle market companies to use private lenders was necessity. As the asset class has matured and lenders have developed relationships and track records, many middle market companies seem to prefer private credit, and tend to work with the same lender multiple times.

Private lenders can offer more flexible funding, the assurance that a deal will close, and shorter timelines to close. In addition, covenants on the loan work to ensure the lender can provide oversight and assistance if a rough patch arises, as what happened during 2020-2021.

A survey by the Alternative Credit Council (ACC) reported that during 2020, private credit manager respondents deployed almost $200 billion in capital, as compared to the $113 billion that had been expected by a similar survey in early 2020. The ACC referred to private credit as a “vital provider of capital support” during economic uncertainty.[footnote val="4" id="4"]

In 2022, E&Y estimated that private credit supported an estimated 1.6 million jobs, contributing $137 billion in wages and benefits and generating $224 for the GDP.[footnote val="5" id="5"]

Private lenders are senior stakeholders in the company, and often require covenants. This means that they can collaborate with company management, get involved early and mitigate potential issues.

Middle Market Loans Performance, 1995 - 2023

Source: Fitch Ratings; Proskauer Private Credit Default Index; Cliffwater Direct Lending Index; as of Q3 2023

Source: Fitch Ratings; Proskauer Private Credit Default Index; Cliffwater Direct Lending Index; as of Q3 2023

Changes to Private Equity May Boost Private Credit Growth

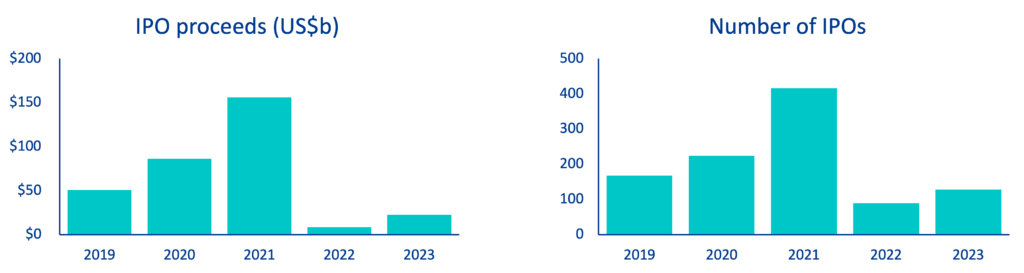

IPOs make headlines but aren’t as common as the media attention makes it appear. In fact, the number of IPOs annually has been shrinking for decades, while the value of the deals and the size of the newly public company have grown. Looking at the data on IPOs tells an interesting story about how companies that go public have changed.

The number of IPO deals plunged 63% from 5,724 in the 1990s to 2,106 in the 2000s. At the same time, the total value of the deals increased from $482 billion to $569 billion.[footnote val="6" id="6"]

The evolving market for IPOs over the 2000s and beyond validates that companies now stay private much longer.IPOs Priced on U.S. Exchanges

Sources: EY analysis, Dealogic Data as of December 31, 2023

Sources: EY analysis, Dealogic Data as of December 31, 2023

How are companies remaining private? Growth in private equity assets under management has been nothing short of explosive, with assets accelerating from $500 billion in 2000 to $13.1 trillion by June 2023.[footnote val="7" id="7"]

Private equity investors bring a long-term focus to company growth and are active partners that can provide assistance and expertise across all dimensions of a company’s business model.

Private equity firms are increasingly turning to private credit to fund buyouts. According to a report by Bloomberg Law, “Over the last five years, more and more private equity firms have turned to private credit sources to fund their leveraged buyouts. Indeed, from 2019 to 2022, private credit firms financed approximately 49% of debt-financed private equity deals valued at $1 billion or greater.”[footnote val="8" id="8"]

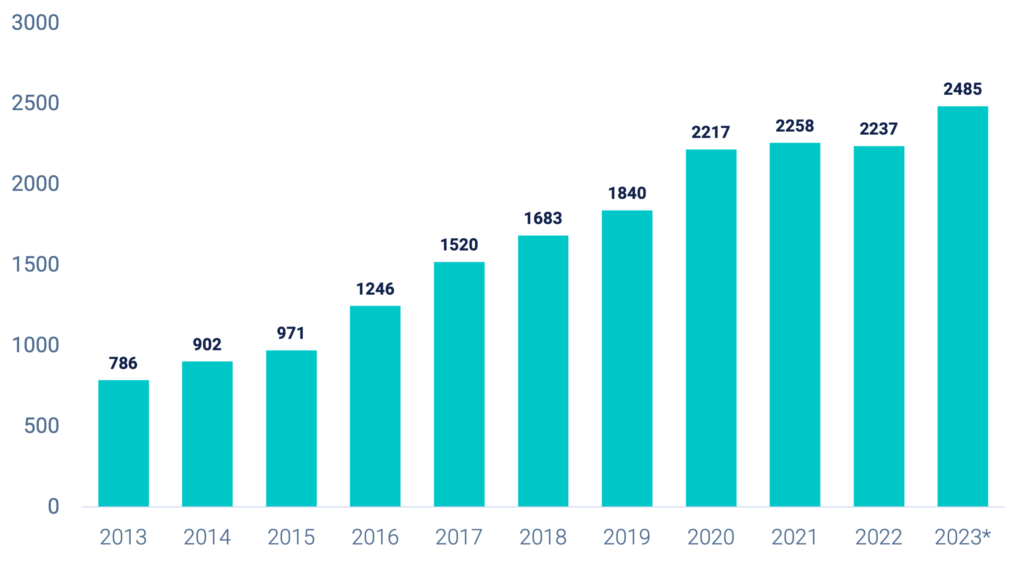

Global Private Equity Dry Powder Trend, 2013-2023 ($B)

Source: Prequin *As of July 3, 2023

Source: Prequin *As of July 3, 2023

The Source of Capital for Private Companies Has Evolved

Private Assets in Tandem Can Mitigate Risks

Institutional private equity owners can also add capital when companies struggle, especially during unexpected downturns. The resiliency of private credit with low default rates throughout 2020-2021 is likely partly due to this feature.

The combination of lenders who can play an active role in helping a company manage debt burdens, along with private equity owners who are willing to contribute additional capital, can result in companies successfully managing a crisis.

From an Investor Perspective

The growth in private credit is also fueled by demand for these assets.

A new business cycle is underway, but until rates, inflation and the labor market have normalized, volatility is likely to be present.

Private debt, through floating rate assets, can help mitigate interest rate risk in a rising rate environment, and has potential to reward investors interest rates remain high.

The asset class is generally less volatile as it is less liquid. Low correlation to traditional credit assets helps with portfolio diversification. These attributes make an argument for considering private credit in a traditional allocation that resonates with many investors.