Why are Institutions Gravitating

to Private Credit?

The vast majority of institutional investors who are allocated to private credit expect to maintain those allocations as part of a long-term investment strategy, according to Preqin. However, a new survey captures the extent that individual investors are allocating to the asset class. According to the research results, 63% of asset managers, hedge funds and wealth managers intend to increase their allocations to private credit.[footnote val="1" id="1"] What is it about private credit that has both major money managers and those managing money for individuals taking notice?

Let’s take a look at five big reasons driving the demand for private credit.1. Illiquid Debt Assets Have Demonstrated a Return Premium Over Their Liquid Counterparts

There exists a significant illiquidity premium that institutional managers seek to exploit. Liquidity may not be a concern for institutional managers with very long-term time horizons. Individual investors who can combine liquid and illiquid assets in their portfolio may also access this premium.

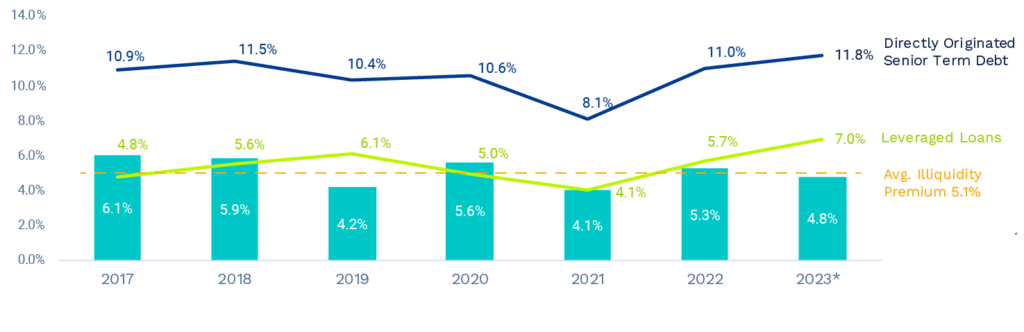

Directly originated senior loans have generated an average 500 bps premium over traded loans since 2017.

Source: Cliffwater Direct Lending Index. Morningstar LSTA US Leveraged Loan Index. *Data as of 9/30/2023.

2. Fixed Income Instruments Struggle in Periods of Rising Rates

The Fed has precipitously raised rates since 2022, and with inflation still above target, Fed messaging is keeping the door open to further increases.

In the last seven periods in which the 10-year Treasury yield rose by 60 basis points or more, bonds have delivered inconsistent returns.

Bond yields reflect the Bloomberg U.S. Aggregate Bond Index Returns. Source: Bloomberg, TIAA Investments.

3. Financial Market Volatility is Back

Market volatility is often measured by the Chicago Board Options Exchange’s CBOE Volatility Index (the “VIX”), which tracks stock market’s 30-day expectation of volatility based on S&P 500 index options.

Sometimes called the “Fear Index”, a reading above 20 signals increased uncertainty and risk.

VIX Volatility Index - Historical Chart

Source: Macrotrends, Note: Interactive historical chart showing the daily level of the CBOE VIX Volatility Index back to 1990. The VIX index measures the expectation of stock market volatility over the next 30 days implied by S&P 500 index options. The current VIX index level as of November 30, 2023 is 12.92 Shaded area represents recession.

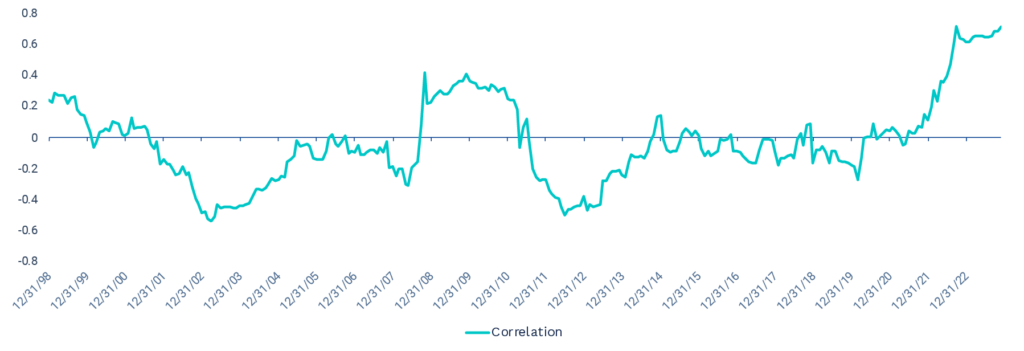

4. Cross-Asset Correlation Can Reduce the Impact of Portfolio Diversification

Private credit assets are not traded on any public exchange, potentially reducing their correlation to broader public markets. True diversification is contingent on the inclusion of uncorrelated assets.

U.S. Stocks, Bonds 90-Day Correlation Since 1999

Correlation between the S&P 500 and the Bloomberg US Aggregate Bond Index. Data from Bloomberg, 1999 -October 2023.

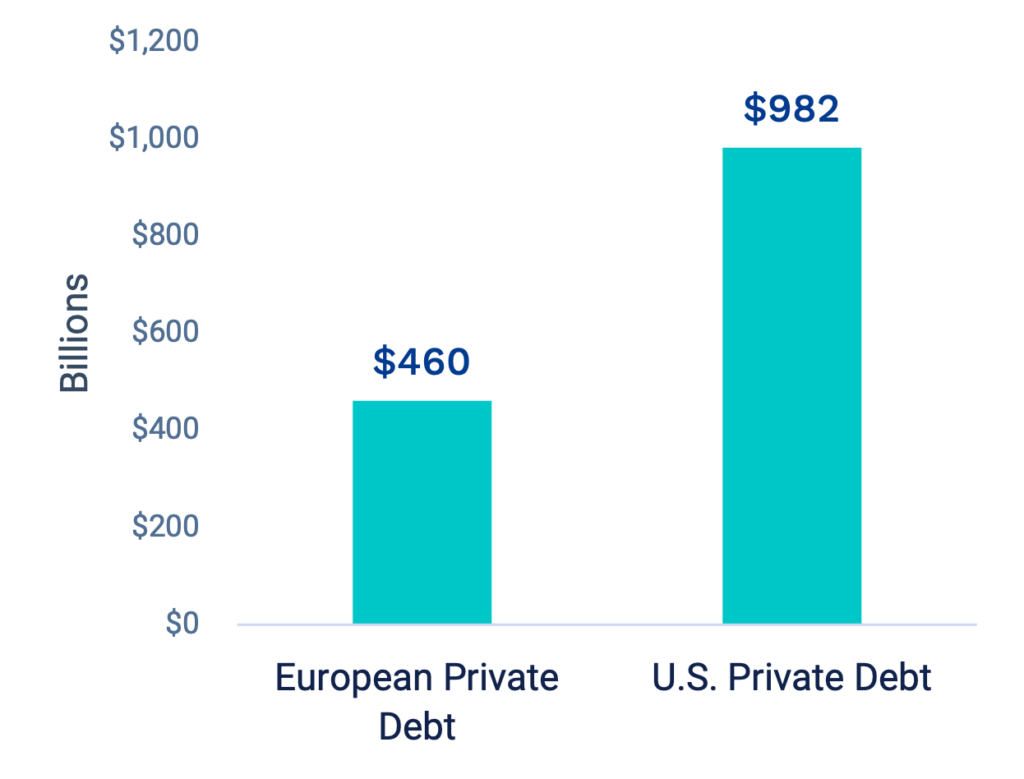

5. The Opportunity Set is Growing Outside of the United States

Private debt markets elsewhere in the world are not as developed as the more mature domestic market. Experienced managers are finding value in the rapidly- growing European arena.

Date for European AUM chart: 1st quarter 2023 Source: S&P Global, Preqin

The structural changes that have led to the emergence of private credit as an established asset class remain firmly in place, with continuing macroeconomic trends supporting the current investment environment. Uncertainty and inefficiencies in the marketplace, enemies of traditional debt investments, create new relative value opportunities across private credit every day. We strongly believe that private credit should not be viewed as a short-term investment thesis or a trade, but rather a long-term investment opportunity in an established and growing asset class.

Risks

The potential benefits of high yield bonds do not come without increased exposure to a few kinds of investment risks. In comparison to investment grade corporate and government bonds, high yield bonds have a higher risk of default and are generally more volatile in terms of their current market value. Over longer investment horizons high yield bonds exhibit premium returns, especially if purchased at a discount to par value. In the short-term however, high yield bonds are subject to swings in value and heightened defaults when economic conditions become less favorable. Because of their risk-return profile, it is imperative that investors are diversifying properly across issuers and market segments. A typical way for investors to access high yield bonds with a degree of diversification is through investment funds that make use of them rather than investing in single bonds.

As with any asset class, there are certain risks associated with private credit. Credit risk is the risk of nonpayment of scheduled interest or principal payments on a debt investment. Because private credit can be debt investments in non- investment grade borrowers, the risk of default may be greater. Should a borrower fail to make a payment, or default, this may affect the overall return to the lender. Further, private credit investments are generally illiquid which require longer investment time horizons than other investments. For these and other reasons, this asset class is considered speculative and may not be suitable for everyone.

To learn more about non-investment grade assets, please contact your financial professional.