From Public to Private: How Advisors Are Using Alternative Investments

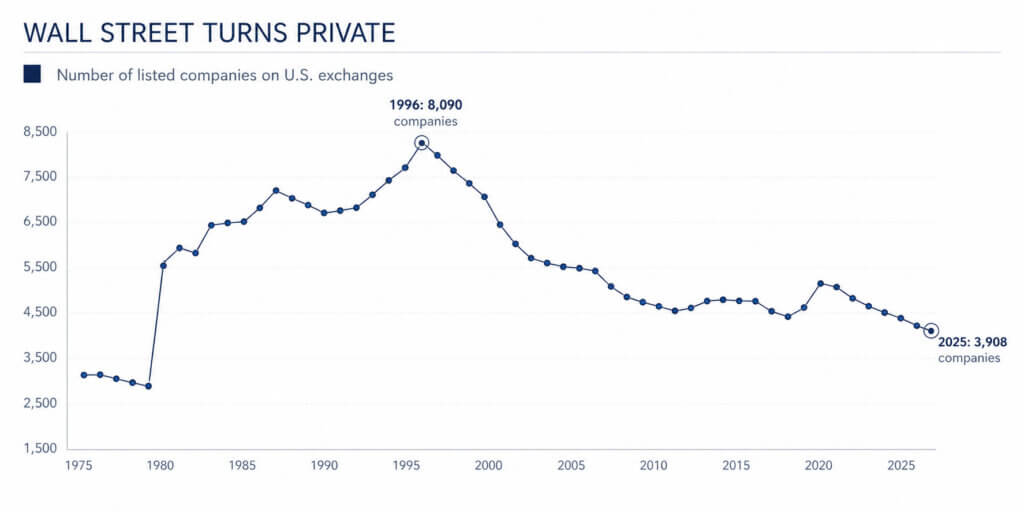

Over the past few decades, the rapid scaling in alternative assets (or alts, as some call them) has expanded the boundaries of investment management. And even though the world has become more public, with social media driving our daily routines into the spotlight, Wall Street has become more private.

Source: Compound Insights, World Bank. Data as of 5/6/2026.

Much of this evolution has taken place with new technology and an ever-changing market structure. Regulations stemming from the global financial crisis pushed fundraising into more opaque channels of the economy. Low interest rates in the 2010s fueled an appetite for riskier endeavors like venture capital. Staying private became a badge of honor for America’s fastest-growing companies, with names like SpaceX, OpenAI and Anduril opting to stay private for years. And everything seems to be investable these days; commodities, art and collectibles can be bought and sold with a few swipes on your phone. Historically complex products have been made simple on both Wall Street and Main Street. Products that were once the province of institutions have become more accessible through new product structures, and a wider range of alternative exposures is now available to self-directed investors and advisory clients. At a time when diversification and edge are scarce, it’s no surprise that Americans are bringing up alternatives to their financial advisors. We wanted to understand the adoption of alternatives among financial advisors — what they’re looking at, where they see growth, and how they’re helping their clients navigate a space that offers less flexibility, but potentially more opportunity. In this paper, we’ll explore how advisors are incorporating alternative investments into their practices and client portfolios. Alternatives, for the purposes of this research, are defined as investments focused on non-traditional assets and strategies, which may behave differently than the broader markets and may help to diversify portfolios. The Survey: This paper presents findings from a joint research initiative developed by CION Investments, Compound Insights, and YCharts. 301 registered investment advisors were surveyed between March 5 and April 7.Setting the standard

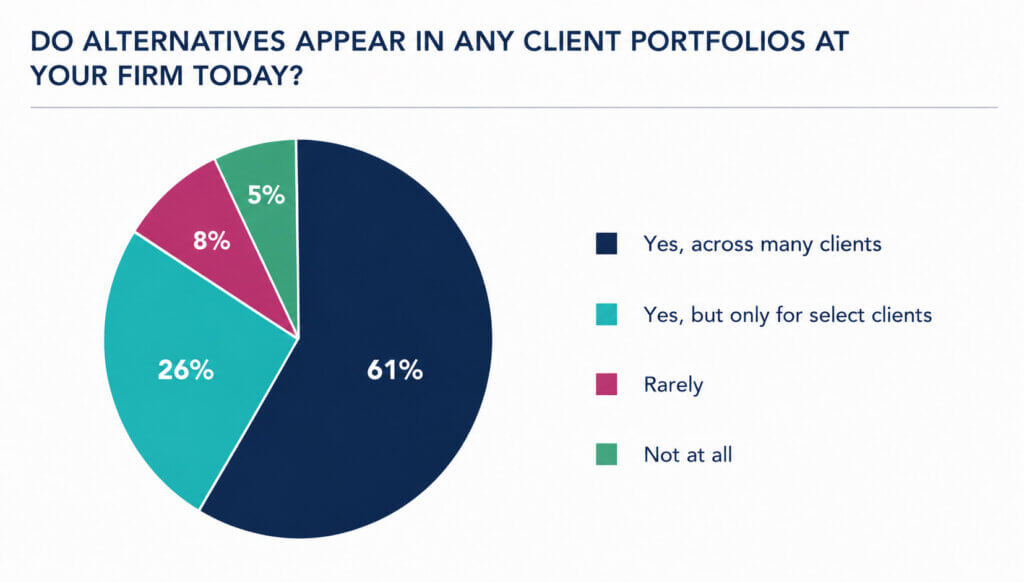

Our survey found broad adoption of alternatives within the standard portfolio, with 95% of respondents reporting that alternatives appear in client portfolios. 61% of advisors reported that alternatives are used “across many clients”, while 26% said alternatives are reserved for select clients.

Source: From Public to Private: RIA Alternatives Survey (2026)

Alternatives aren’t just a garnish in portfolios, either. Alternative allocations are at least 10% of total assets for 68% of clients deploying them, and 9% of clients have allocations greater than 20%. While advisors clearly welcome the use of alternatives, they’re approaching the allocation to alternatives in different ways. There’s a wide spectrum, from firms explicitly recommending an allocation to alternatives, to passively managing clients with existing allocations to alternatives. The data shows that growth in alternatives adoption has been driven by interest from all parties. Advisors and investment professionals have become more knowledgeable, and so have their clients. Whether advisors choose to recommend alternatives or not, the number of questions from clients and prospects who are curious and see alternatives as a potential differentiator will likely increase. Advisors will need to be able to speak to the merits and limitations of alternatives, and their firm’s stance on them. Also, as an advisor it’s important to calibrate the right portfolio for a client’s goals and needs. If a new client comes in the door with an alternatives allocation you don’t agree with, you often can’t just exit the positions and dust your hands off. The lack of transparency in some private assets and structures can lead to dramatic changes in value and over-concentration in certain investments. While a client may not be able to check market values or access their investment as easily, the position in alternatives may be significant enough to influence goals and performance.Choosing the right investment

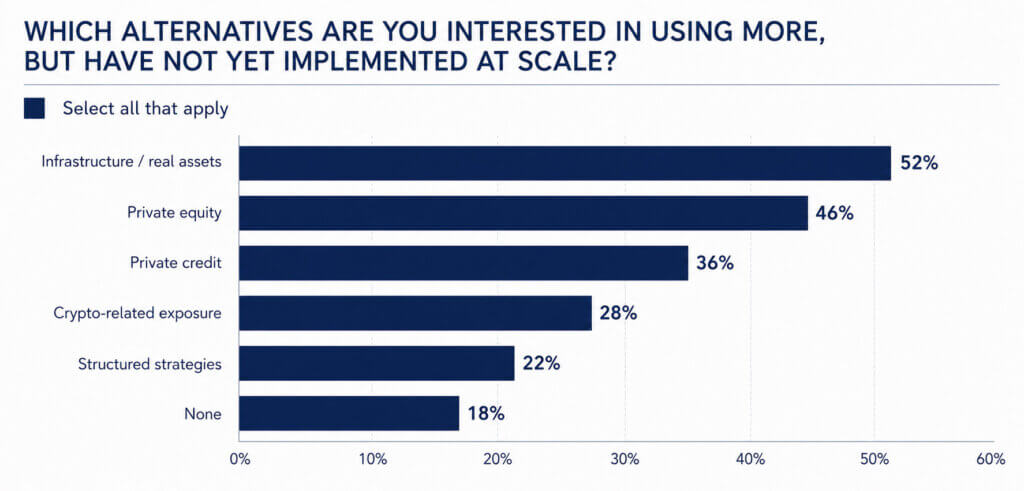

This study was conducted during a period of notable scrutiny for several alternative asset classes. Private equity and credit have seen increased attention, with negative outcomes on specific deals making headlines and driving media attention, whether warranted or not. In our survey, we asked advisors about which specific investments they’re interested in using more, but have not yet implemented at scale. Infrastructure and real assets led the field at 52%, followed closely by private equity at 46% and private credit at 36%.

Source: Compound Insights, From Public to Private: RIA Alternatives Survey (2026)

The preference for real assets makes sense. Real estate and infrastructure are well-known, tangible investments. Business investment is soaring, and data center financing has become a popular way to gain exposure to the AI theme. Real estate opportunities may come in all shapes and sizes, but many investors can understand the concept of investing in a slice of a shopping mall or apartment complex. Private equity and private credit are newer, more abstract concepts for a wealth management portfolio. However, they are becoming an important part of our economy: the swath of businesses that can’t, or choose not to, fundraise through traditional channels. Advisors know which categories they would like to lean into further; the question is what’s kept them from doing so. When asked what best explains the interest-versus-implementation gap, advisors most often cited liquidity concerns (61%), followed by complexity of structures (46%) and client comprehension (46%). Each of these answer choices presents a struggle many advisors are familiar with. Successfully implementing alternatives requires an advisor to understand the strategy as well as the structure it is available in, and to be able to convey that thoroughly to a client. It is critical to ensure that there is a match between what the client wants to achieve, and what their needs and comfort level are. Given the positive sentiment around the asset classes that have been caught in an unprecedented level of media scrutiny, it seems clear that advisors’ and their clients’ interest has not meaningfully abated. Advisors are correct in citing liquidity concerns; the limited liquidity of some structures is necessary to ensure the manager can execute on a long-term strategy. This requires the advisor to be certain that the investor’s liquidity needs are taken into account before investing. Similarly, while the potential return of some strategies is linked to the complexity premium, it requires more work on the part of the advisor to explain this adequately to an investor. It’s important to highlight that just 14% of advisors cited the lack of a portfolio role when explaining why they haven’t implemented certain alternatives more broadly. Alternative investments can serve as performance enhancers, but their utility doesn’t end there. They can provide benefits to a portfolio beyond its profit-and-loss line: tax benefits, uncorrelated returns, yield, exposure to tangible assets, etc. And in an environment of entrenched inflation, relatively high interest rates, and ever-changing tax policy, a successful portfolio involves much more than just beating a benchmark.The complex becomes simple

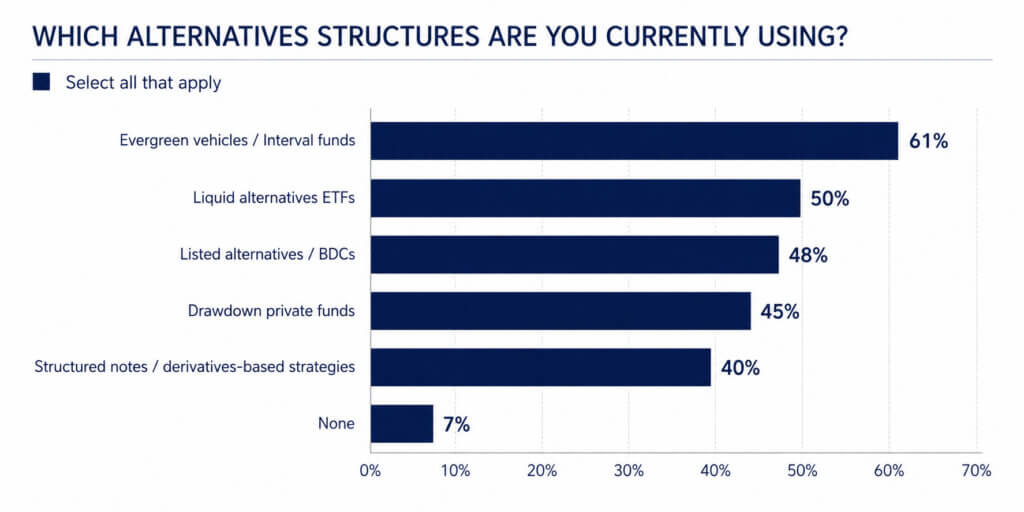

One trade-off advisors have to contend with is the balance between simplicity and efficiency. Once upon a time, alternatives required a certain level of wealth and expertise, plus the foresight to wait years – even decades – for any payoff. Luckily, the space has evolved beyond a one-size-fits-all approach. Today, there’s a wide variety of investment vehicles, including public market solutions that basket up derivatives, private investments and structured options strategies to bring alternatives to the masses. Advisors seem to be making use of these new tools. When asked about which vehicles they use to invest in alternatives, 61% of advisors told us they use selected evergreen vehicles/ interval funds and 50% said they use liquid alternatives ETFs.

Source: Compound Insights, From Public to Private: RIA Alternatives Survey (2026)

Liquid alternatives ETFs and listed alternatives/BDC have been the classic channel for everyday investors to snap up alternatives exposure. Drawdown funds typically require a capital commitment that is called over time. Evergreen and interval funds can offer transparency, simple tax treatment and a daily NAV, but liquidity is limited and redemptions may be prorated. Structured notes are highly complex and can have lofty minimum investments as well. Some firms have developed structures that wrap private assets in public market formats. More traditional alternative investment structures often carry accreditation requirements or high minimum investments that limit the eligible client base. For those clients, public market vehicles may represent the most practical route to alternatives exposure. Access has been simplified, yet the underlying risk remains. So today, advisors have a choice to make. You either utilize the traditional alternative investment structures and learn how to offer them in the right situations, or you opt for public market vehicles in familiar structures. Drawdown and evergreen funds often provide the cleanest exposure to private investments, but the strategies require expertise to manage. Plus, advisors must be careful about manager selection and spend time explaining the limitations of the structure to clients. Listed alternatives and liquid alternatives offer immediate liquidity and more transparency, but the exposure to the underlying strategy can be diluted by the structure. You can choose to offer different solutions for different client tiers, but it’s important that you understand and communicate the tradeoffs for each.Practical takeaways for advisors

- Adopt a common language. An allocation to alternatives often isn’t as straightforward as it seems. Alternatives are a wide universe of investments, including anything from private assets to complex derivatives and niche collectibles. Before you advise clients on alternatives, learn your firm’s specific stance on what alternatives are and how they’re treated. It’s important that you and your colleagues are speaking the same language.

- Implement a clear strategy. If your firm doesn’t have a clear strategy around managing alternative assets, it’s time to roll up your sleeves. Alternatives adoption is growing fast, and you’ll need to be able to speak to the asset class at a minimum and articulate your firm’s stance. This includes views on specific investments (private equity/credit, commodities, structured notes) as well as the vehicles used to invest (funds, ETFs, other offerings).

- Understand the why. Alternatives are becoming a part of the mainstream investing conversation. And as they get more popular in the U.S., you’ll have to contend with different beliefs and narratives about them. Some are true, but many aren’t. Don’t fall prey to the narratives. Lean on your investment team to understand the benefits and drawbacks of different investments, including what you gain and give up through prioritizing liquidity and transparency.

- Prioritize thorough research. Private assets seem to be past the COVID era of easy money. Interest rates are historically higher than in recent years and capital has become selective. While due diligence and manager selection are always important for alternative investments, they’ve become more of a differentiator for performance. Invest in research, whether you’re recommending alternative investments to clients or simply responding to opportunities they bring you.

- Be an intentional communicator. Alternative investments may not always be as liquid or transparent, but they can often influence a client’s goals long before a planned exit. Have a plan for monitoring alternative investments and educating the client on their use and purpose. There’s a delicate balance between too little and too much.

- Find the shades of grey. People tend to see the world in black and white, yet investing and portfolio management operate in shades of grey. Oftentimes, what is considered suitable for one client doesn’t work for another, and the use cases for alternatives are vast. Instead of blindly recommending an allocation or closing your mind off to the entire space, consider how alternatives can help different types of clients achieve specific desired outcomes.

In the end, the question for advisors isn’t whether alternatives are worth allocating to. Rather, how they can enhance a portfolio, and what tradeoffs clients are willing to accept.